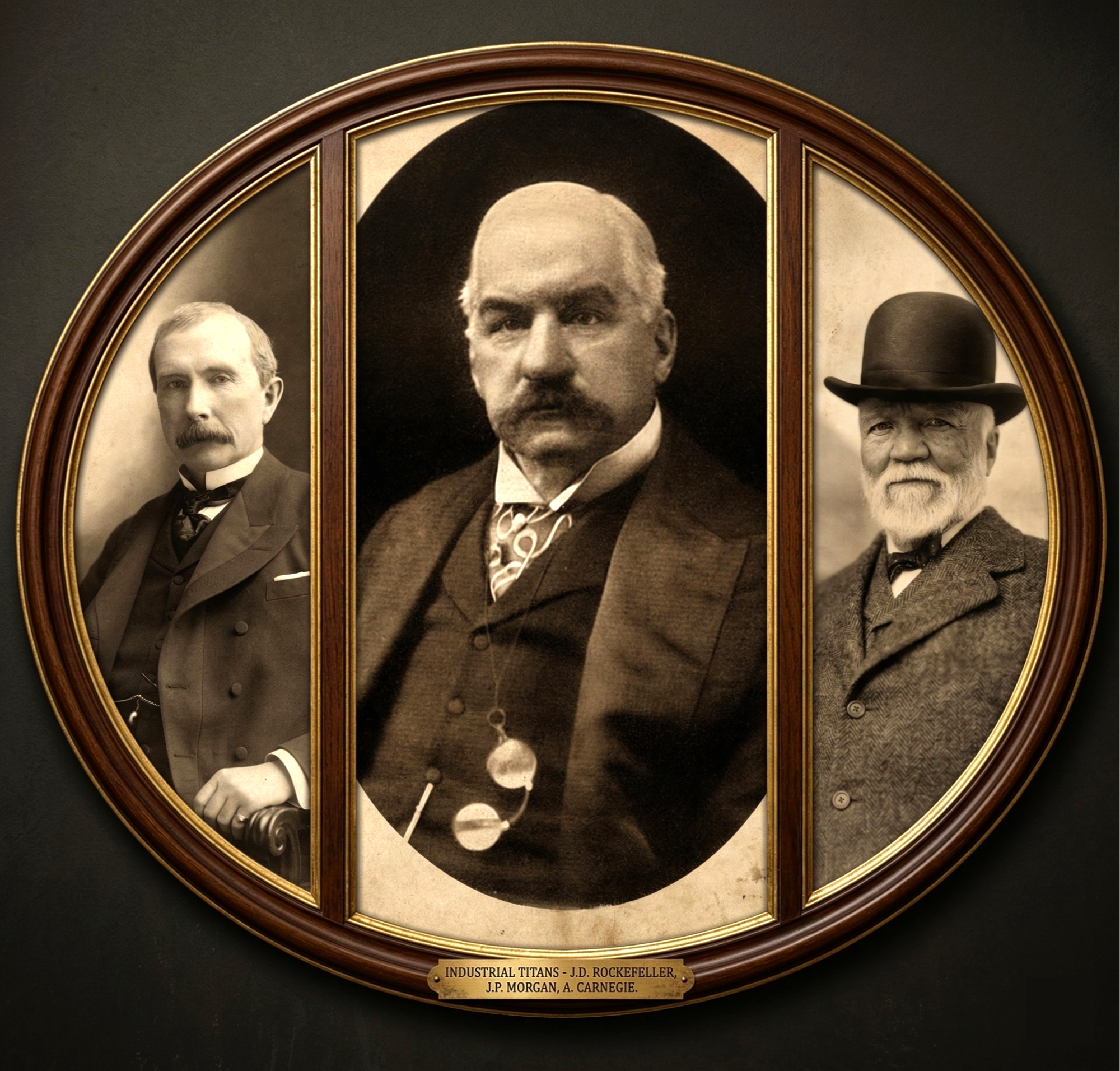

The Men Who Owned the World | Titans of Industry, Then and Now

The reporters had just arrived. They were there to cover the forced sale of Standard Oil assets following the Supreme Court's landmark antitrust ruling earlier that year. They expected anger. The spectacle of a great empire being dismantled by order of the highest court in the land, decades of building undone within hours.

What they found was that John D. Rockefeller was playing golf.

He had been playing golf, in fact, when the original ruling came down that May. A caddy had brought him a telegram on the fairway at the golf club. Rockefeller read it, folded it, slipped it into his pocket, and made his next shot. Afterward, he mentioned to a playing partner that the Standard Oil trust had just been dissolved. Then he suggested they play another nine.

It was a performance, and it was calculated to project the serene indifference of a man who could not be touched. But it was also, in a deeper sense, simply true.

When the company was broken into thirty-four independent firms, Rockefeller held shares in all of them. The aggregate value of those shares doubled, then tripled, over the following decade. The man the government had broken remained, without serious competition, the wealthiest human being on earth.

The age that produced him had produced others like him. It would be a long time before their like appeared again. Or so people thought.

The World They Built

The Gilded Age. A term Mark Twain coined as a critique, not a compliment. This was a reference to the application of a thin layer of gold on an otherwise ordinary surface. It ran roughly from the end of the Civil War in 1865 to the early years of the twentieth century, and it was a period of economic growth so astonishing, so concentrated, so ruthless, that we are still arguing about it today.

The United States transformed itself, in a single generation, from a largely agrarian nation into the world's leading industrial power. The railroads tied it together. Steel girded it. Oil lit it and later moved it. And coal-fired everything in between.

The men who seized control of these industries did so in conditions that no longer exist and probably cannot exist again. A vast, resource-rich continent is being industrialized for the first time. The federal government was too small and too philosophically reluctant to regulate what was happening. A legal framework that had not yet invented the concepts of antitrust law, securities regulation, and labor protections, which would eventually constrain the largest accumulations of private power.

It was, in the most literal sense, a world without many rules. The strongest and most ruthless players wrote them as they went.

Andrew Carnegie came to America from Scotland at twelve with nothing. By the 1890s, Carnegie Steel produced more steel than the entirety of Britain. He had achieved this not through superior technology alone, though he was genuinely brilliant, but through a relentless, almost predatory efficiency. He cut costs past the point his competitors thought possible. He drove wages down and production up. He bought out rivals, sometimes charitably, sometimes not. When his workers struck at the Homestead Steel Works in 1892, Carnegie retreated to his Scottish castle and left his manager, Henry Clay Frick, to handle it. Frick hired three hundred Pinkerton guards, armed them, and floated them toward the plant on barges. The ensuing battle on the riverbank left several dead. The union was broken. Carnegie, when pressed, claimed he didn’t know anything about it. Historians don’t believe him, and neither did the public at the time.

He sold Carnegie Steel to J.P. Morgan in 1901 for $480 million, roughly $17 billion in today's money, and spent the rest of his life giving it away. He built 2,509 public libraries. He funded concert halls and universities. He wrote essays arguing that the wealthy had a moral obligation to redistribute their fortunes before they died. "The man who dies rich," he declared, "dies disgraced." He meant it. He gave away approximately ninety percent of his total wealth before his death in 1919.

This raises an uncomfortable question. Was Carnegie truly a villain or a hero? His libraries are still standing. So is the memory of Homestead. The honest answer is probably that the philanthropy does not redeem the exploitation, but it does complicate it. The workers who were shot on the riverbank are not made whole by a library in Pittsburgh. And yet the libraries exist, and people use them, and something real was built with money that was taken. History rarely offers the clean moral account we want. Carnegie was not the villain we need him to be, and he is not the hero he tried to become. He is, more usefully, an illustration of what concentrated power can do to a person, and how the justification for one’s actions can be influenced by such power.

Rockefeller built his empire through a different method. Not brute force, exactly, but something more patient and arguably more devastating. He negotiated secret railroad rebates, arrangements with railroad companies to carry his oil at lower rates than his competitors paid, while also receiving kickbacks on his competitors' shipments. This gave Standard Oil a cost advantage that no rival could match or even understand, because the arrangement was secret. This made the free-market idea and concept irrelevant. No one could compete with the secrets or the size of Standard Oil. Competitors would find their margins inexplicably crushed, their customers vanishing, their businesses slowly starving. Then a Standard Oil representative would appear at the door with an offer to buy them out. Most sold. Those who refused generally went bankrupt. By 1882, Standard Oil controlled approximately ninety percent of the refining capacity in the United States. It set the price of oil not just in America but, effectively, in the world.

Busting the Trusts

Theodore Roosevelt became president in 1901, the same year Carnegie sold his steel company to Morgan. The timing was not coincidental in its significance. The era of unchecked industrial consolidation was running directly into an era of political reaction, and the impact would reshape the American economy.

As shared in a podcast a few weeks ago, Roosevelt is often remembered as the great trustbuster, and the label is partly deserved. His administration filed forty-four antitrust suits and broke up the Northern Securities railroad monopoly in a 1904 Supreme Court ruling that genuinely shocked Wall Street. But his actual philosophy was more nuanced. He believed in distinguishing between good trusts, large companies that had grown through genuine efficiency and superior products, and bad trusts, companies that had used illegal or unethical methods to crush competition.

The government's role, in his view, was not to punish success. It was to regulate power. To ensure that private economic strength did not overwhelm public governance.

It is a distinction that sounds obvious until one tries to apply it, at which point it becomes extremely difficult. Concepts and partnerships are tested at the moment money changes hands. The test never ends.

Roosevelt’s successor, William Howard Taft, was also an aggressive trustbuster. Ninety antitrust suits in four years, compared to Roosevelt's forty-four in seven. Woodrow Wilson added the Federal Trade Commission and the Clayton Antitrust Act to the regulatory arsenal. But it was Roosevelt who established the template: the federal government had not just the right but the obligation to intervene when private economic power threatened the public good.

The tools they forged in the first decade of the twentieth century became the instruments through which the Gilded Age's most extreme concentrations of wealth were constrained. The age of the absolute industrial titan, the man who could control an entire industry by will and cunning alone, was ending. Labor law, securities regulation, the graduated income tax, and the growing strength of organized labor all began to work, gradually and imperfectly, to distribute the fruits of industrial free markets more widely.

It took fifty years.

And then, in a different industry, in a different century, the cycle began once again.

Commanding New Heights

Jeff Bezos founded Amazon in a garage in Bellevue, Washington, in 1994. He was thirty years old, a former hedge fund manager who had quit his job, driven across the country with his wife MacKenzie, and begun writing code for an online bookstore.

He would later admit that the bookstore was never the point. Books were a start. A product category with millions of titles, predictable shipping weights, and no major online competitor. Amazon was always intended to be something larger: an everything store, and then something larger than that.

Three decades later, Amazon controls approximately forty percent of American e-commerce. Its cloud computing division provides the infrastructure on which a substantial portion of the modern internet runs, including, in some cases, the websites of companies that compete directly with Amazon's retail business. Its logistics network is massive. It is a retailer, a technology company, a cloud provider, a media studio, a pharmacy, a grocery chain, a device manufacturer, and more, all at once.

At his peak net worth, he has more personal wealth than the GDP of most countries.

The mechanisms differ across companies, and the distinction matters. Google's dominance is in attention. Meta's power is in networks. Apple's leverage is the tollbooth, where every application on the world's most widely used computing device passes through a single distribution channel, and Apple takes a cut of every transaction that crosses it. Amazon is a logistics and a marketplace at once: it built the infrastructure that smaller retailers depend on, and then became their most direct competitor. Each is a different kind of chokepoint. Each has its own kind of power. What they share with Rockefeller is not the method. It is the underlying logic: find the place where everything must pass through and own it.

The threat of new entrants and competition can be offset if the leading company gets big enough, has scalable processes, and in the rare event that another organization becomes a genuine threat, it can just be purchased and assimilated into the whole. Rockefeller controlled oil refining. The technology giants control platforms.

That said, and this is very important, there are differences worth noting. Carnegie and Rockefeller operated in industries that involved back-breaking physical labor, dangerous working conditions, and the kind of obvious human exploitation that generates political outrage. The technology industry's products are, at the consumer level, often free and frequently convenient. Working conditions are not dangerous – at least not in the same way as they were for Carnegie and Rockefeller employees – and are subject to federal oversight. Weekends exist. There are no child laborers. In fact, most of these tech giants have substantial family incentives, such as paid maternity leave for the father as well as the mother. Though the environment and working conditions have changed for the better, such improvements often mask similar practices as the industry titans of old.

When Standard Oil squeezed competitors off the market, the victims were other businesses; the consumer often saw lower prices. When Amazon uses pricing algorithms to undercut competitors on its own marketplace, the immediate effect for the shopper is also often lower prices. The harm, in some cases, is to competition itself. “Some” is a key note here. Amazon is able to lower prices because it has engineered and reengineered its logistics to be as inexpensive as possible. In the same vein, it negotiates with suppliers and, due to its volume, can lower the cost of the individual product. The savings are passed down to the customer. The same thing happens with Walmart, Costco, and other big-box stores. Similar things happened with Carnegie and Rockefeller, not all the time, not every time, but at those times that it seemed appropriate to them.

The philanthropic tradition has continued as well, in forms Carnegie would have recognized. Bill Gates left Microsoft to dedicate himself to the Gates Foundation, which has spent tens of billions of dollars on what Gates defines as “global health and education”. Bezos has pledged billions to climate change initiatives. Elon Musk has argued that his accumulation of capital is in service of a larger mission: the survival of human civilization through the space colonization of Mars.

Carnegie, reading this, would have recognized the structure of the argument, if not the specific ambition.

He might also have recognized something else: the tendency of very wealthy men to define the public good in terms that happen to align with their own interests and preferences, and the difficulty, in any era, of holding private power democratically accountable when that power is vast enough to shape the political environment itself.

History Rhymes

Mark Twain called the original Gilded Age "gilded" because it means to coat something unimpressive with gold. He was writing about the 1870s. The description aged well.

The Gilded Age produced real, insane amounts of wealth, and some of that wealth translated into genuine improvements in ordinary life. The price of oil dropped by eighty percent during Standard Oil's dominance. Carnegie steel built the bridges and skyscrapers that defined modern American cities, which spurred additional demand and supply of the automobile. The railroads that the robber barons built, sometimes corruptly and brutally, tied the continent together and made national commerce possible.

But the Gilded Age also produced a level of inequality that somewhat destabilized the republic itself. By 1890, the wealthiest one percent of Americans controlled more wealth than the vast majority of the population combined. Senators were openly referred to as the property of particular railroad companies. The gap between what the economy produced and what ordinary workers received grew so large, and stayed that way for so long, that when the Progressives finally arrived with their antitrust suits and regulatory reforms, they were acting as repairmen, trying to patch a system that had been stretched nearly to a breaking point.

The parallels to the present are imperfect, as all historical parallels are. The technology economy is genuinely different from the steel economy in important ways. The political and legal tools available to regulators today are different from those available to Roosevelt and Wilson. The global nature of the modern digital economy creates challenges that simply did not exist when all of Rockefeller's refineries were in Ohio and Pennsylvania.

And yet.

The Federal Trade Commission has begun filing major antitrust suits against Google, Meta, and Amazon. The European Union has moved more aggressively still, levying billions in fines against American technology companies and passing comprehensive regulatory reform designed to constrain these companies in ways that echo, at least in spirit, the Sherman Antitrust Act of 1890. Congress has held hearing after hearing, with senators questioning technology executives in scenes that carry an unmistakable echo of the Senate hearings on railroad monopolies a century earlier.

History is a cycle, and in the long drama of industrial free markets and governance, it has a way of returning to the same arguments, the same tensions, the same fundamental questions. How much private power is compatible with a free republic? Who decides when an accumulation of wealth has become an accumulation of political power? How is that defined? Who defines it? Why are they the authority to do so? What does a government owe its people when a handful of private actors can shape the conditions of daily life more decisively than any elected official?

Rockefeller finished his round of golf, got into his car, and went home to his estate. He lived for another twenty-six years, long enough to see the automobile replace the oil lamp and make his fortune relevant in an entirely new way. He died in 1937, at ninety-seven, still the richest man in American history.

Somewhere right now, in a home office or a garage or a college dormitory, someone is building the next thing. The names will be different. The industry will be different. The arguments, a generation from now, will be familiar.